2025: The year digital compliance became strategy

2025 was the year digital compliance became strategy. As the global pivot from paper to structured electronic data accelerated, tax authorities worldwide decisively moved closer to a real-time reality.

Here is your comprehensive look back at the landmark e-invoicing and e-reporting developments of 2025.

2025: The year digital compliance became strategy

In 2025, e-invoicing evolved from a back-office IT project into a core business strategy. The primary driver remains the VAT Gap, the multibillion-euro difference between expected and collected tax revenue. Governments are no longer content with summary-level periodic reports - they now demand granular, invoice-level data as it happens.

However, forward-thinking businesses are discovering that this “digital burden” is actually a springboard for operational excellence. By moving beyond mere compliance, companies are leveraging structured data to automate accounts payable, reduce manual errors, and dramatically improve cash flow cycles. This shift represents a fundamental change in how we view tax technology: VAT compliance is no longer just a cost of doing business, but a genuine opportunity to transform and optimize the enterprise.

The Heavy Hitters: Major rollouts in 2025

Germany: The reception revolution

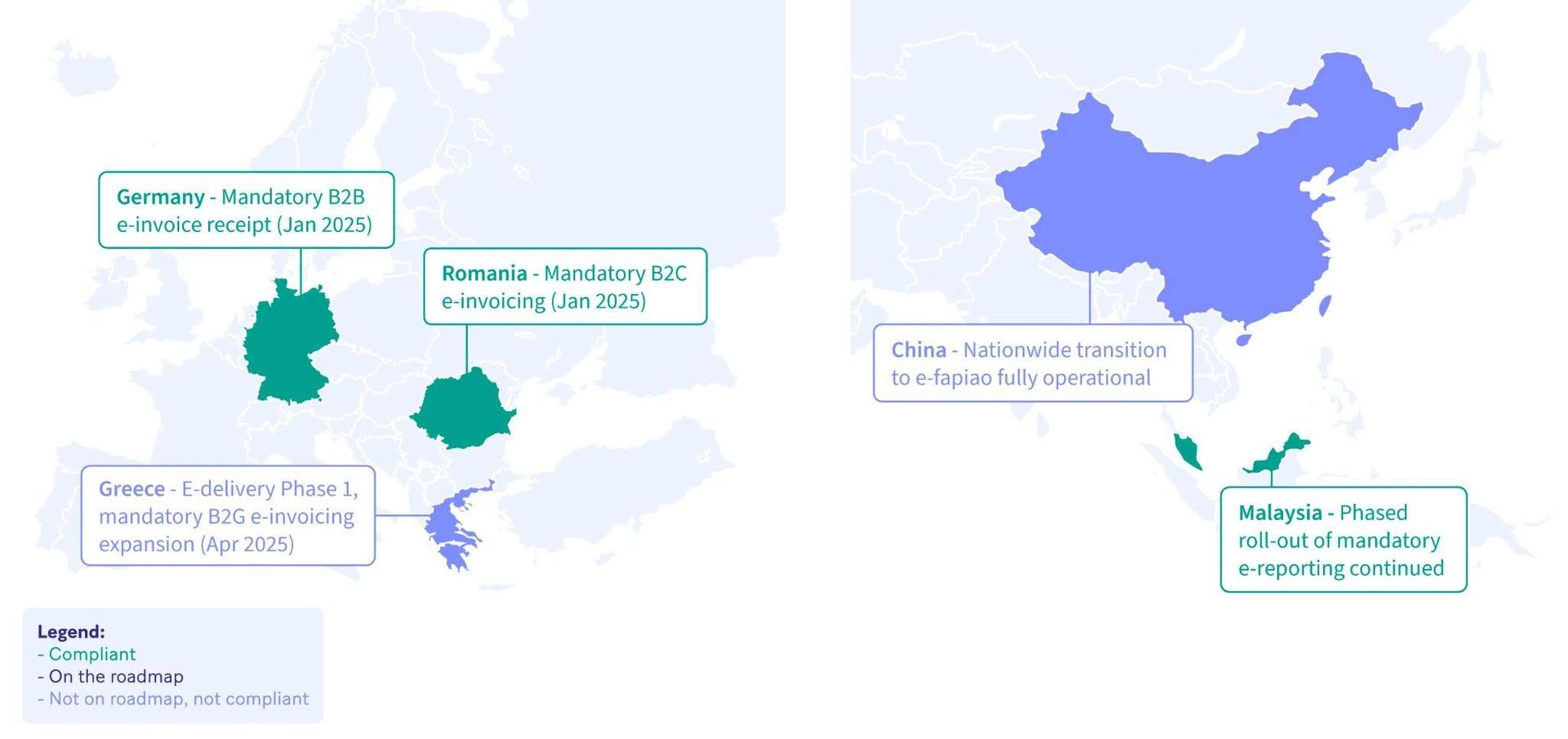

On January 1, 2025, Germany fundamentally flipped the script on B2B invoicing. Under the Growth Opportunities Act (Wachstumschancengesetz), the “primacy of paper” ended. While businesses have until 2027–2028 (depending on business size) to start issuing e-invoices, every German business was required to be able to receive structured e-invoices (like XRechnung, the German CIUS, or ZUGFeRD, a commonly used German equivalent identical to the French CIUS Factur-X) from day one of 2025.

Romania: Closing the B2C loop

On January 1, 2025, Romania significantly increased the stakes by enforcing mandatory B2C e-reporting nationwide. All domestic B2C transactions must now be reported via the RO e-Factura platform, supplementing the B2B mandate that has been in place since early 2024. This move is part of a broader strategy by the Romanian Ministry of Finance to combat tax evasion in sectors susceptible to fraud and to create a fully transparent digital tax ecosystem.

Greece: Beyond invoicing to e-delivery

Greece advanced its digital transformation by extending the myDATA system into the logistics sector. In April 2025, the country launched the first phase of its e-delivery mandate, requiring businesses with revenues over €200,000 to report transport details in real-time. Simultaneously, Greece expanded its B2G mandate, requiring all government expenditures over €2,500 to be invoiced electronically through the Peppol network, and secured EU approval to enforce a full B2B mandate using the EN 16931 standard.

Malaysia: Strategic relaxation for SMEs

Malaysia successfully launched Phase 2 (taxpayers with annual turnover or revenue of more than RM 25 million) of its MyInvois mandate at the start of 2025, and Phase 3 (for taxpayers with an annual turnover or revenue of more than RM 5 million) in July, bringing mid-sized businesses into the fold. However, the most significant news came in December 2025, when the government announced a decision to ease the burden on smaller enterprises. The e-invoicing exemption threshold has been raised from RM 500,000 to RM 1 million, meaning taxpayers with an annual turnover below this new limit will be exempt from mandatory compliance beginning in 2026.

China: The nationwide e-fapiao reality

China reached a historic milestone in 2025 by completing the nationwide transition to the e-fapiao system. This government-controlled electronic invoice serves as an official tax receipt validated in real-time, giving the State Administration of Taxation (SAT) direct visibility over domestic B2B and B2C transactions. By late 2025, the e-fapiao became the predominant invoicing format, effectively eliminating separate e-reporting deadlines through a “clearance-upon-issuance” model.

New frontiers: Global compliance takes hold

Beyond the major rollouts, 2025 saw a critical mass of smaller, but equally significant, mandates take effect, confirming that the digital compliance shift is truly a global phenomenon spanning Europe, the Caribbean, Asia, and beyond. A few examples include:

Indonesia’s Coretax revolution: In January 2025, Indonesia launched its new Coretax system, making real-time e-invoicing and clearance mandatory for all VAT-registered taxpayers (PKP). The mandate covers B2B, B2G, and exports, requiring businesses to use a central portal for validation.

Dominican Republic mandate expansion: The Caribbean region saw progress as the Dominican Republic expanded its mandate on May 15, 2025, requiring all medium-sized taxpayers to issue and receive e-invoices for both B2B and B2G transactions.

Digital Bookkeeping takes hold in Denmark: On January 1, 2025, Denmark enforced Phase 2 of its Bookkeeping Act, mandating that all medium and large companies utilize digital bookkeeping systems that meet strict new integrity and traceability requirements.

The Great Wait: Notable postponements

If the last few years have proven anything, it’s that digital transformation is rarely a straight line. Technical complexity and business readiness led to several strategic pauses in 2025:

Poland: Although the mandatory start of the KSeF e-invoicing system was postponed from 2024 to 2026 by an announcement made in late 2024, 2025 marked the year the framework was finalised. On August 27, 2025, the President signed the legislation confirming go-live dates of February 1 and April 1, 2026. The law introduced major technical updates (including KSeF 2.0 and the FA(3) schema) and additional transition relief, such as a penalty-free period until the end of 2026 and a delay of the requirement to include the KSeF invoice number in bank payments until January 1, 2027.

Spain: In 2025, attention focused on preparing billing software for the upcoming VERI*FACTU requirements, while the long-awaited nationwide B2B e-invoicing mandate under the Crea y Crece (Create and Grow) Law remained without confirmed implementation dates. Ongoing regulatory delays pushed market expectations for mandatory B2B exchange increasingly toward 2027. This timeline was further reinforced when the official announcement regarding the VERI*FACTU rollout was itself delayed late in 2025, pushing its expected start dates toward 2027 as well.

Latvia: The mandatory B2B e-invoicing and reporting mandate, initially expected in 2026, was delayed in 2025 to give businesses more time to prepare. Following a brief period of legislative proposals, Parliament formally adopted new deadlines in June 2025. The new timeline sets the compulsory domestic B2B e-invoicing and reporting date for January 1, 2028, while clarifying that mandatory B2G transaction reporting to the State Revenue Service (SRS) will commence on January 1, 2026.

Future mandates confirmed

2025 was also a year of legislative groundwork for the years ahead:

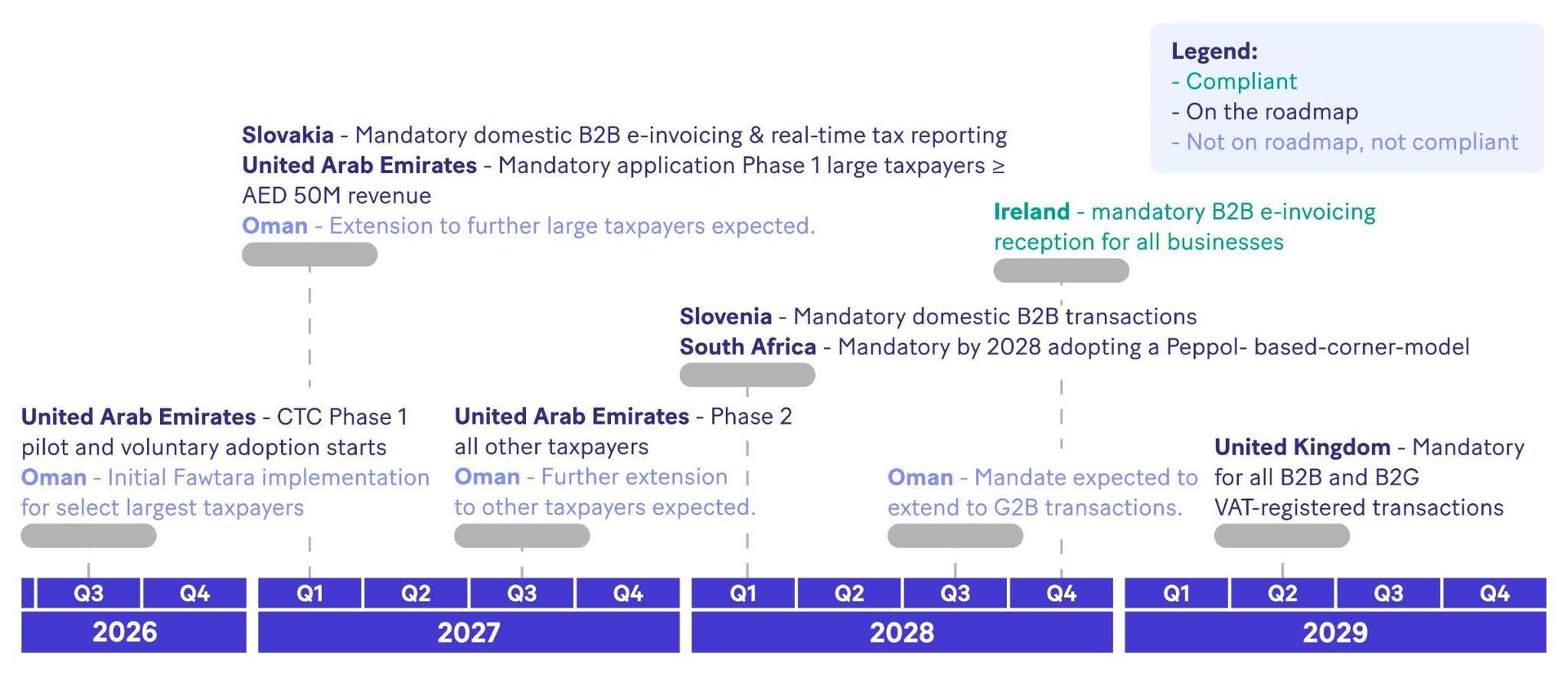

United Arab Emirates (UAE): The UAE transformed its e-invoicing vision into law on September 29, 2025, with the issuance of Ministerial Decisions 243 and 244. These decisions confirm a phased implementation of its e-billing system starting with a voluntary pilot in July 2026, with mandatory compliance for large businesses (revenue ≥ AED 50M) starting January 1, 2027. The system will be built on the Peppol PINT AE standard, with Accredited Service Providers (ASPs) being a cornerstone of the DCTCE model.

Slovakia: The mandatory B2B electronic invoicing and reporting mandate was fully approved by the National Council on December 9, 2025, setting the go-live date for January 1, 2027. By adopting a 5-corner model comparable to the Peppol-based approach, Slovakia's system will rely on Accredited Service Providers (ASPs), referred to as “Digitálni poštári” (“digital postmen”), to facilitate secure exchange and real-time reporting to the tax authority.

Oman: In late 2025, the Oman Tax Authority (OTA) solidified the implementation of its Fawtara e-invoicing initiative. The mandate will proceed in four phases, beginning with a pilot for 100 large taxpayers in August 2026, and progressively extending to all VAT-registered businesses by August 2027. The model also relies on the use of Accredited Service Providers for secure exchange.

Slovenia: In 2025, Slovenia made a definitive shift towards mandatory B2B e-invoicing, adopting the Act on the Exchange of Electronic Invoices and Other Electronic Documents (ZIERDED) on October 23. This Act establishes January 1, 2028, as the go-live date for all domestic B2B transactions, providing a transition window for private sector alignment with B2G standards. Notably, the final Act abandoned the previously proposed real-time reporting requirement to FURS in favor of a decentralised exchange model that encourages the use of registered service providers (“ponudnikov e-poti”, or loosely translated, e-route or e-path providers) for converting and exchanging e-invoices.

Ireland: Following an extensive public consultation, the Irish Revenue formally published its roadmap, “VAT Modernisation: Implementation of e-invoicing in Ireland”, in October 2025. Ireland will follow a phased approach, starting with large VAT-registered corporates on November 1, 2028. The mandate will combine e-invoicing and real-time reporting, leveraging the Peppol network to reach full ViDA alignment by July 2030.

United Kingdom: In a historic move, the UK government, on November 26, 2025, officially confirmed during Budget 2025 that e-invoicing will become mandatory for all B2B and B2G VAT-registered transactions starting April 1, 2029. The UK has signaled a preference for a decentralized “4-corner” Peppol-based model.

South Africa: Legislative groundwork for the “Tax Administration 3.0” transformation was laid in 2025 with the Draft Tax Administration Laws Amendment Bill (TALAB). Following late-2025 public consultations, the South African Revenue Service (SARS) confirmed a roadmap toward a mandatory rollout by 2028, with strong signals of adopting a Peppol-based 5-corner model.

The “Class of 2025”, specifically the United Kingdom, Ireland, Slovenia, and the United Arab Emirates, signifies a notable global shift. By confirming mandates that extend several years into the future, these nations are offering businesses the long-term predictability required for substantial ERP and financial system overhauls. The prevalence of the Peppol/Decentralized model in these confirmations indicates a growing global consensus on balancing tax transparency with business efficiency.

The Policy Rationale: CTC vs. Peppol

The “Model Wars” became more nuanced in 2025, evolving from a simple choice into a clear strategic division that dictates the future of global tax enforcement. The debate is now less about “if” e-invoicing is mandatory and more about the fundamental philosophy of the compliance infrastructure. Two dominant approaches emerged:

Clearance-based Continuous Transaction Control (CTC): This traditional model, popular in Latin America and countries like Italy and Poland, requires the invoice to be “cleared” or validated by the tax authority, often via a central government system, before or while it is sent to the customer. It provides maximum, real-time control for the state.

The Decentralized Exchange Model (5-Corner-based): This framework focuses on interoperability. It allows businesses to use their own Certified/Accredited Service Providers (CSPs/ASPs) to exchange invoices securely, utilizing networks like Peppol. The key distinction lies in the role of the Tax Authority, which, in this model, acts as a connected “5th corner” that receives or extracts data in (near-)real-time, crucially without blocking the business-to-business invoice flow.

Side-by-side visual comparison of the CTC vs. decentralized exchange models

Side-by-side visual comparison of the CTC vs. decentralized exchange models

Examining the current status of e-invoicing mandates, both those already in effect and those that by 2025 were confirmed for (future) implementation, reveals a clear strategic division that reinforces established trends. The Clearance CTC model remains the preferred choice in high-tax-gap jurisdictions, particularly in Latin America and parts of Europe. This model prioritizes state visibility and real-time control. In contrast, the Decentralized Exchange model, specifically the five-corner/DCTCE approach, is becoming the de facto standard in Europe and among key global trade partners in the Middle East, such as the United Arab Emirates (UAE), favoring market interoperability and faster business integration.

To understand the core differences between these two models and others, read our dedicated blog post “The e-invoicing maze: Navigating global compliance models” here.

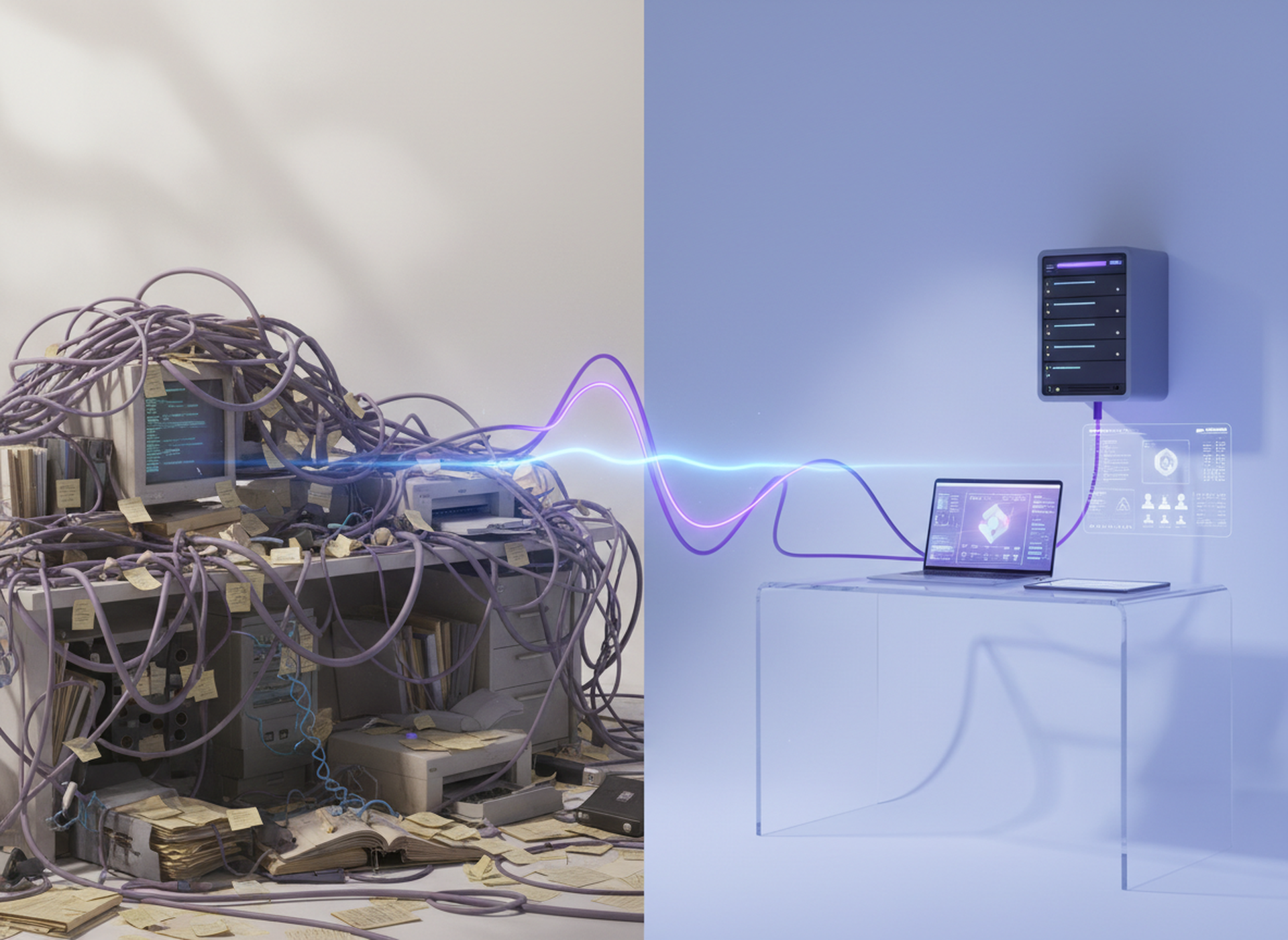

Challenges and technology enablers

The transition hasn't been without pain points. Businesses in 2025 struggled with:

Legacy integration: Upgrading ERP systems to produce XML data instead of just visual PDFs.

Digital signatures: Navigating the complex requirements for qualified electronic signatures (QES), which vary by country.

Fragmented formats: Managing UBL, CII, and various national XML flavors simultaneously.

Technology to the rescue: 2025 saw a boom in Cloud Middleware and API-based compliance layers. These tools act as a “universal translator”, allowing a company's ERP to send one data stream that is then formatted and routed correctly to meet the specific mandate of each country.

Non-mandated trends: The US & voluntary adoption

Interestingly, the United States saw an uptick in voluntary e-invoicing in 2025, even without a federal mandate. Large enterprises began adopting Peppol-based standards to streamline their accounts payable processes, demonstrating that the advantages of e-invoicing, such as faster payments and fewer manual errors, are appealing even without the prospect of a tax audit.

Looking ahead to 2026

If 2025 was the year of “receiving” and “planning”, 2026 is shaping up to be the year of “issuing”. With France, Belgium, Croatia, and more, all hitting major milestones next year, the “Tornado Phase” of global e-invoicing is officially here.

Stay ahead of the curve: Follow us on LinkedIn for more timely updates on these shifting mandates and sign up for our monthly newsletter to get compliance summaries delivered straight to your inbox. Explore our compliant e-invoicing solutions today and connect with our local team to learn more.

Danielle Kiener

Lead Key Account Manager, Banqup Group

Danielle has 15 years of experience in customer relationship management within invoicing and financial administration. She currently works in Geneva, supporting global customers at Banqup Group and helping multinational companies digitise their processes. Over the years, she has been closely involved in the digital transformation of invoicing, including leading e-invoicing initiatives across the EMEA and Asia-Pacific regions for a major multinational. Her extensive experience means she’s always up to date on the latest e-invoicing regulations and changes around the world.